Crypto's First Killer App and the (Regulated) Future of Finance

It's not irony that stablecoins are crypto's first major innovation since BTC and ETH, it's simply the direction the space was always headed

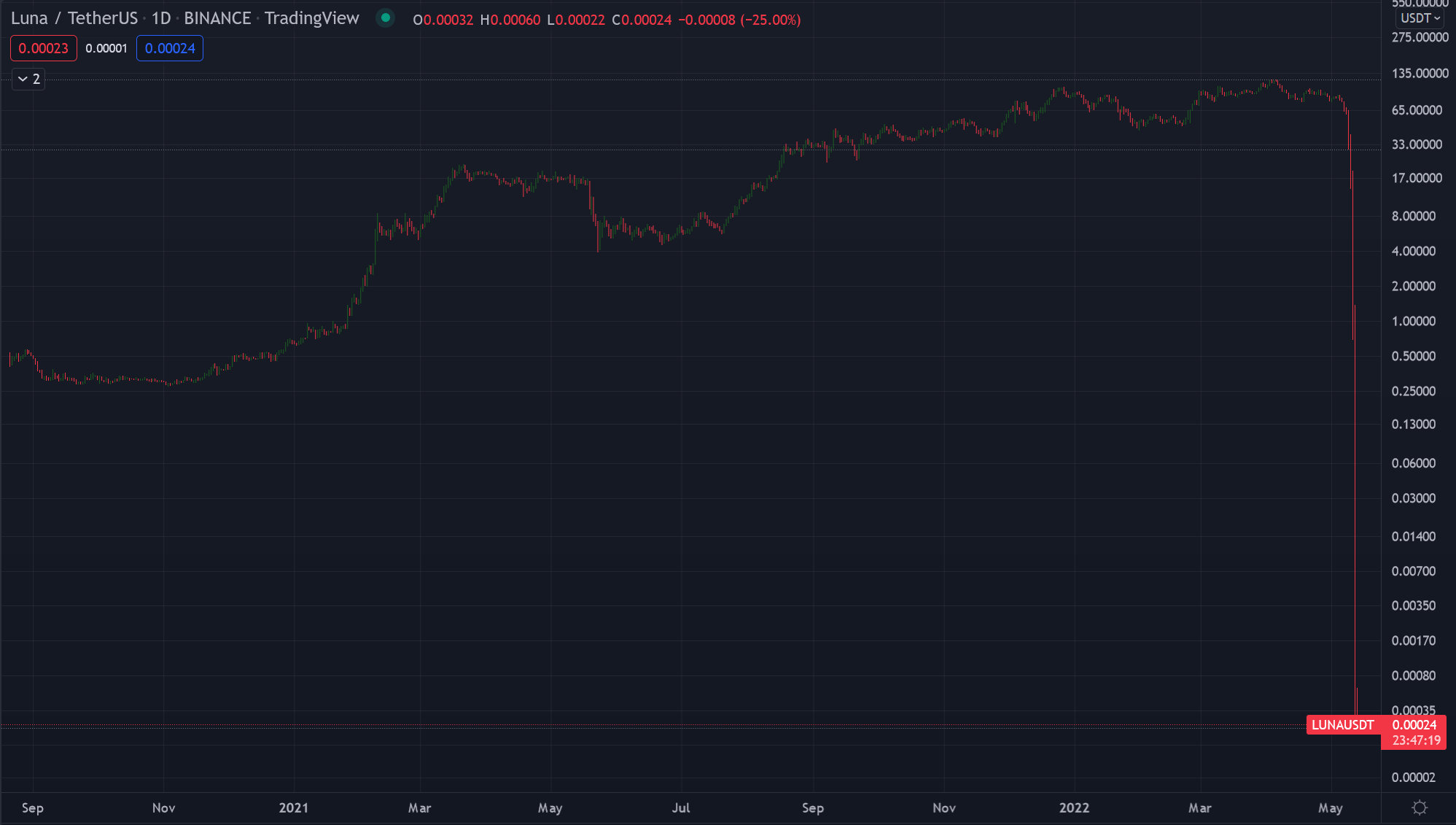

Earlier this year, two multi-billion dollar cryptocurrencies evaporated practically overnight, leaving a wake of retail investors completely screwed over by both a regular speculative cryptocurrency (LUNA) and a currency they were assured was always worth $1 no matter what (UST), called a stablecoin.

Tether is the first and most notorious stablecoin, and I wrote in 2018 for Paste Magazine about how it pretty obviously seem(ed?) to be a way to print money out of thin air and artificially boost the price of Bitcoin. USDC is now the most rapidly adopted and most trustworthy stablecoin, and it is issued by Circle and Coinbase, two publicly traded companies.

So what makes a stablecoin trustworthy?

Same thing that makes any currency issuer trustworthy: whether the issuer has money in the bank to exchange one stablecoin for $1. USDC has its reserves routinely audited, and the problem with Tether was that it never agreed to audits and its potential holdings were extremely questionable given the amount of money they were issuing—but it is now under the microscope of the state of New York—and so if there are any current treasury shenanigans being perpetrated by Tether, I am certain that New York will tell us about it. These two are trusted stablecoins because they have redemption systems that large and small firms access each and every day to move money between the crypto ecosystem and the fiat system.

Crypto’s Version of E-mail

In 1994, if you would have described why TCP/IP protocols were important to someone, they’d probably look at you like you were speaking gibberish. A few years later, people were using e-mail and the opacity of the technology melted away as the utility of the product made itself clear. I believe there is a similar dynamic currently developing between blockchains and stablecoins.

Stablecoins are a massive innovation for crypto because they allow you to interact with financial blockchain applications without having to expose yourself to the extreme swings of the market, and they provide access to dollars for anyone with an internet connection. Some may ask why we need to build payment rails outside of established systems, but in the age of mass surveillance, that question should answer itself.

Not to mention that sending money through the existing banking system can be a pain, especially any kind of large amount. Anyone who has bought a house should understand the value of having a payment rail that can settle and verify near-instantly with little hassle and minimal fees.

Outside the United States, Bitcoin has been a lifeline to less advantaged parts of the world because it has created financial infrastructure that did not exist there before, and it provided people with a way to preserve their savings in the face of inflation and hyperinflation. These innovations by the king of crypto paved the way for the space’s next big step forward: providing people with the security and stability of a decentralized financial system without taking on the risk of its economic downside.

Argentinians use stablecoins to protect themselves from an unstable local currency. The Chinese use stablecoins to send remittances and get around capital controls. Both stablecoins and BTC and ETH have helped political dissidents fund their operations fighting the authoritarian regime in Belarus, and they have provided funds to the Ukrainian army as they struggle to escape from under the thumb of Russian influence on multiple fronts. The examples of crypto’s usefulness are all around you, you just have to get outside our bubble of 330 million people.

That doesn’t mean there aren’t use cases for it in the United States. I sold merchant accounts for the banks, and I can tell you first-hand how inefficient and corrupt our current payment rails are. The banks shave roughly 3% off the top of the economy just for settling your transaction every time you swipe a debit or credit card (and pay people like me to tell merchants they’re paying 1.5%). Stablecoin fees are far lower than that (Ethereum fees, now that’s another more complex story), and having trusted issuers of crypto-dollars has proven to be a big step forward in how people send money to each other around the world. It doesn’t take a whole lot of imagination to understand how crypto can help Americans, and that’s even before you get to the fact that Bitcoin and Ethereum had more up time last year than the Federal Reserve’s ACH system.

The “Future of Finance” Needs Regulation

I can already hear the libertarians howling, but if you truly want the public to trust this brand-new financial system, you’re not going to get that without governments providing a framework to get them to trust it (not to mention for those who are in it just for the wealth and desperately want the bankers to buy our coins, the only way that happens is if crypto is properly regulated).

Crypto needs to understand that (smart) regulation is a net long-term good. The LUNA fiasco set mainstream crypto credibility back years. The space needs help legitimizing itself and (smart) government stablecoin regulation is one of the fastest ways to reestablish some serious credibility in the eyes of the public.

Asserting that stuff like LUNA shouldn’t exist should not be controversial to those whose goal is to make crypto as broadly popular as possible. It was not an unforeseen accident of an earnest attempt at financial innovation, and a death spiral was always going to happen to both LUNA and UST as soon as the markets faced a severe downturn. Plenty of people in crypto said so well ahead of the implosion, and LUNA’s founder, Do Kwon, even dared billionaires to try to exploit the very obvious vulnerability he had created.

Now what made it particularly exploitative was hooking this system up to a free flow of people chasing 20% interest on UST deposits in Anchor Protocol, as it advertised supposed risk-free riches to the masses in order to help maintain the Rube Goldberg machine of (temporary) profitability constructed by its incredibly dickish founder who is extremely deserving of all the shit that comes his way from this (funnily enough, his name spells “now KO’d” in reverse).

If you’re offering 20% interest on stablecoins, you have to explain to people how their money is at risk because “free 20% interest” is another phrase for ponzi scheme (although during the frothy times in bull runs you can get really good interest like this from legitimate parties because conditions are filled with such easy money that degenerate traders can borrow at like 80% APY to speculate on altcoins and still be profitable). The vast majority of the time however, any advertised rate that high in crypto carries far more risk than the normal ~2% you can expect at the handful of big well-established players (which is a really great rate when you compare it to what banks give you for your “savings” account).

Not every yield farming outlet in crypto is a ponzi—the crypto economic model is centered around the constant distribution of coins and so there is plenty of room for legitimate economic activity and innovation on this front—but crypto must find a way to make important distinctions around the risk of its financial products. Proper “staking” will always entail some level of risk and what that is must be accurately communicated to users. Regular people shouldn’t be expected to poke and prod every protocol in extreme detail before trusting it—that’s a recipe to keep crypto in the kiddie pool and away from the ocean of capital around the world.

As far as crypto’s budding crown jewel goes, the issue now is what should constitute a “stablecoin.” USDC and Tether both utilize the (mostly) safe bank model, where they hold cash and cash-like instruments that they routinely exchange for the stablecoin, while DAI is an algorithmic model utilized by the Maker protocol that has worked very well to date. The publicly-audited bank model seems safe enough and DAI has blazed a trail for algorithmic stablecoins, but there needs to be some sort of standard set so people can trust stablecoins to actually be stable, and they will then take their rightful place alongside all other sorts of trusted money sent across the globe.

But it must be regulation that helps provide crypto with a proper long-term framework, and it and can’t be an onerous bill that either just tries to ban it entirely or is like the block-headed law passed by the Democrats last year where they effectively said that using a Metamask extension was punishable by public execution—plus all crypto is banned except for the Bitcoin mining industry that is conveniently moving from China to the U.S. at the exact same time as the passage of the bill.

I know many of my lefty allies will disagree and say “no the laws trying to ban it are good,” but crypto is a global market with deep roots in Europe, Asia and South America, and any ban by the United States government would just ban the United States from crypto. The cat is out of the box and our government isn’t that powerful anyway (not to mention that crypto is specifically designed to try to resist state-sponsored attacks). You’re stuck with crypto for the foreseeable future whether you like it or not.

The Future of Finance

Value is relative, money is just a medium for us to trade value, and there are plenty of other ways than just fiat currency for people to exchange value. If I give you my collectors comic book for your collectors baseball card in order to both complete our respective collections, we are exchanging value just like if we had sold them to each other with USD or EUR or JPY or GBP or AUD or CAD or CNY or some combination as the middleman.

So it makes sense in the age of the internet that internet-native currencies like BTC and ETH have sprung up. The web is an easy way to exchange value, but value is relative around the world and trading value through various fiat currencies isn’t always easy. The subsequent problem crypto had to address was how to square the volatility of the coins with the technical stability of the chains. Stablecoins emerged and are now exploding in places like Argentina where serious inflation runs wild and demand for dollars is practically infinite.

When my sister studied abroad in Buenos Aires, she was directed to a black market where she could exchange her dollars for Argentine pesos at well above the going exchange rate. It was a seedy area of town and looking back she’s lucky she made it out with the bounty she came for. It’s unquestionable that stablecoins will not only make these kinds of transactions spurred by economic devastation safer, but they also spread the dollar to every corner of the world with an internet connection. Stable payment rails and stable currencies are something we take for granted in America, and these innovations are a powerful tool for people across the world in broken economies stuck under the boot of western imperialism.

Crypto began as an a rallying cry to overthrow the existing financial system and to a degree it has lost its way. It is now overwhelmed by moon bois obsessed with their (unrealized) generational wealth while shilling their supposedly genius portfolios to a public still uncertain about what the heck this all is. Bitcoin’s genesis block from 2009 has a Financial Times headline about bank bailouts coded into it, and given that another round of bailouts has begun in England (with more across the world likely on the way as economic conditions continue to deteriorate), it’s high time that crypto returns to its roots from the Great Recession. The fact that its first killer app is something that is always going to be $1 is a great step in that direction towards its revolutionary ideals and away from the moon bois, and it needs to keep that energy flowing through this bear market.

Crypto was never going to actually overthrow the system (in the short to medium term at least), but it did communicate a powerful message that most everyone agrees with according to opinion polling: the existing financial system is unfair and rigged in favor of the mega-rich. This was evident during the crash of 2008 when Lehman Brothers did to the global economy what LUNA did to crypto earlier this year, and it is even more obvious today that the existing system is horribly inefficient as we are more leveraged now than we were then. Many systemic financial problems exposed by 2008 have gotten worse, not better.

Add inflation as the end result of years of said unaddressed systemic issues, a COVID supply-chain shock, and a Fed looking backwards while driving the world into a recession to try to crush inflation that may have already peaked, and there is more reason than ever to not trust the existing system that is controlled by central and commercial banks and the entrenched powers they serve. We need an alternative medium to globally transact and preserve economic value that we can use should another 2008-style event or worse occur (and uh, look around you folks, it’s not looking great!). Even if disaster does not strike, simply just having a secure method to transact away from the prying eyes of the NSA and its Five-Eyed allies is a product worth creating.

Any alternative must integrate with the existing financial system in some way (it’s called an “on-ramp” for a reason), otherwise the alternative will never grow to the size it aspires to be, and it especially won’t overthrow the existing system all on its own. But crypto can’t reform our financial system unless crypto itself is reformed. Schemes like LUNA simply cannot exist unless they are correctly labeled as the casino games savvy crypto investors know them to be.

Crypto needs to stop being known as the land of fraud, waste and retail investor scams. It should follow the lead of stablecoins and expand a system focused less on the price of coins and more on the utility of blockchains. Blockchains have immense potential to transform the global economy and change the way that we do business, regardless of the price of its coin (and whether every single product needs a coin with monetary value attached to it is a legitimate question many in crypto should ask themselves).

Crypto began as a revolutionary cry, but now is publicly defined by its obsession with wealth. I admire a lot of the work still being done in the space, as every cycle makes significant technological progress on the previous one—but I am dismayed at how much of the culture has devolved into a tacky parody of what it was created to ameliorate. Crypto has the opportunity to make the world a more equitable place—and stablecoins will be at the forefront of that transformation—but it will never happen if everyone thinks that it all just looks like LUNA.